Universal Insurance Holdings, Inc. Reports Fourth Quarter and Full Year 2017 Results

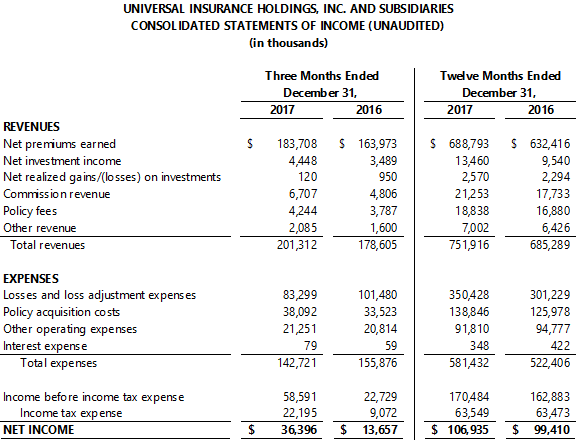

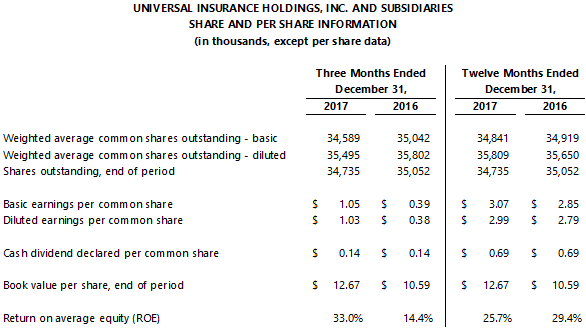

Fort Lauderdale, FL, February 20, 2018 – Universal Insurance Holdings, Inc. (NYSE: UVE) today reported net income and diluted earnings per share (EPS) of $36.4 million and $1.03, respectively for the fourth quarter of 2017. For the year ended December 31, 2017, net income was $106.9 million while diluted EPS was $2.99.

Universal Insurance Holdings, Inc. Chairman and Chief Executive Officer Sean P. Downes commented: “In the months since Hurricane Irma made landfall, Universal has demonstrated the true value of our business model. Our comprehensive reinsurance program substantially limited net losses incurred from one of Florida’s largest hurricanes in over a decade, our vertically integrated structure produced various income streams in the months following the storm, and our superior claims handling and catastrophe response teams delivered excellent service to our policyholders, closing claims in a timely and orderly manner. Our underlying results were also strong, highlighted by continued organic growth and underwriting profitability, as we maintained underwriting discipline and adhered to our strategy of producing profitable and rate-adequate business, with meaningful growth in both Florida and our Other States book, and steady expansion of our Universal DirectSM platform. Our balance sheet remains solid. During the fourth quarter we strengthened both current and prior accident year loss reserves, and we believe our loss reserves are appropriately set at current levels. We delivered a 33.0% ROE for the fourth quarter and a 25.7% ROE for 2017, results that validate our unique business model, and we remain well positioned to deliver outstanding value to shareholders throughout 2018 and beyond.”

Fourth Quarter 2017 Highlights

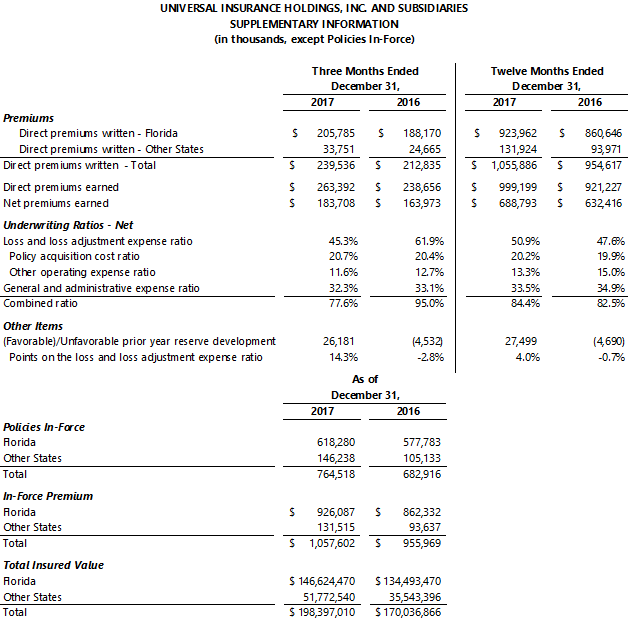

- Premium Growth Continues – Direct premiums written grew 12.5% in the fourth quarter, with 9.4% growth in Florida and 36.8% growth in Other States; Universal DirectSM contributed to growth in all geographies. We began writing in New York during the quarter, and now write in 16 states with licenses in 4 additional states.

- Strong Underwriting Profitability – The fourth quarter net combined ratio was 77.6%, improved from 95.0% in the prior year’s quarter (which included Hurricane Matthew) with reductions in both the loss and LAE ratio and the G&A expense ratio. The current quarter includes a $9.2 million (5.0 points) loss and LAE benefit from Hurricane Irma due to reinsurance recoveries recognized during the quarter, and approximately $35.0 million (19.1 points) of estimated pretax profit relating to additional income generated by our service company subsidiaries following the storm. The current quarter also includes $26.2 million (14.3 points) of prior accident year reserve strengthening and $18.3 million (9.9 points) of current accident year reserve strengthening.

- Solid Balance Sheet – Book value per share grew 3.7% from September 30, 2017 (19.6% from year-end 2016) to $12.67. Our investment portfolio is stable and composed of high quality securities, we have minimal debt or goodwill, and we are protected by a comprehensive reinsurance program, which performed as expected and designed following Hurricane Irma. We took action to strengthen both current and prior accident year reserves during the fourth quarter, driven primarily by Assignment of Benefits (AOB) related claims within our Florida book, including the increased litigation frequency experienced during 2017 surrounding the AOB issue. We believe our loss reserves are appropriately set at current levels.

- Focused on Shareholder Returns – Return on Average Common Equity (ROE) was 33.0% for the fourth quarter of 2017 and 25.7% for the full year 2017. We paid total dividends of $0.69 per share during 2017 for an annual dividend yield of 2.8%, including a special dividend during the fourth quarter. We repurchased 10,000 shares for $0.3 million ($25.71 per share) during the fourth quarter and 770,559 shares for $18.1 million ($23.54 per share) during the full year; $19.8 million remains on our buyback authorization.

Fourth Quarter 2017 Results

Direct premiums written grew 12.5% from the prior year’s quarter to $239.5 million, with 9.4% growth in our Florida book and 36.8% growth in our Other States book. Our organic growth strategy within our home state of Florida remains on track, and our organic geographic expansion efforts within our Other States book continue to produce results. We note that fourth quarter 2017 results include an increased level of both new and renewal business within our Florida book surrounding Hurricane Irma, in part related to a temporary emergency order by the Florida Insurance Commissioner suspending policy cancellations and nonrenewals by insurance companies for a period following Hurricane Irma (please see “Hurricane Irma Overview” section for additional details). For the quarter, net premiums earned grew 12.0% to $183.7 million.

Commission revenue grew by 39.5% versus the prior year’s quarter to $6.7 million, driven largely by the benefit of approximately $2.0 million of fee income related to reinstatement commissions received by Blue Atlantic Reinsurance Corporation during the fourth quarter of 2017. Policy fees grew by 12.1% versus the prior year’s quarter to $4.2 million, driven by increased premium volume. Other revenue grew 30.3% versus the prior year’s quarter to $2.1 million.

The net combined ratio was 77.6% in the fourth quarter of 2017 compared to 95.0% in the prior year’s quarter. The increase in underwriting profitability was driven by both a reduction in the loss and loss adjustment expense ratio and the general and administrative expense ratio.

The net loss and LAE ratio was 45.3% in the fourth quarter of 2017, compared to 61.9% for the prior year’s quarter. The main drivers of the change in the loss and LAE ratio are as follows:

- The current year’s quarter included a benefit of $9.2 million (5.0 points on the loss and LAE ratio), reflecting recoveries received from our reinsurance program related to Hurricane Irma (please see “Hurricane Irma Overview” section for additional details), compared to net losses and LAE of $26.6 million (16.2 points) in the fourth quarter of 2016 related to Hurricane Matthew.

- Fourth quarter 2017 results include $26.2 million (14.3 points) of unfavorable prior year reserve development, related to accident years 2013, 2015, and 2016, driven primarily by Assignment of Benefits (AOB) related claims within our Florida book, including the increased litigation frequency experienced during 2017 surrounding the AOB issue. Fourth quarter 2016 results included $4.5 million (2.8 points) of favorable prior year reserve development.

- Fourth quarter 2017 results include $18.3 million (9.9 points) of current accident year reserve strengthening, driven primarily by AOB related claims, as discussed above. The prior year’s quarter included $16.8 million (10.2 points) of current accident year reserve strengthening.

- We believe our loss reserves are appropriately set at current levels, as we note that the 2013-2016 accident years are well seasoned at this point and have been increased meaningfully from initial picks, while the current accident year loss pick includes added conservatism above the actuarial best estimate.

The net general and administrative expense ratio was 32.3% in the fourth quarter of 2017, compared to 33.1% for the prior year’s quarter, as a modest increase in the policy acquisition cost ratio was more than offset by a decline of the other operating expense ratio. The net policy acquisition cost ratio was 20.7% compared to 20.4% in the prior year, while the net other operating expense ratio was 11.6% compared to 12.7% in the prior year.

Additionally, our service company subsidiaries generated substantial additional revenues following Hurricane Irma that led to approximately $35.0 million of estimated pretax profit generated by service company subsidiaries during the fourth quarter of 2017 (please see “Hurricane Irma Overview” section for additional details). These benefits were reflected in both loss adjustment expenses and general and administrative expenses.

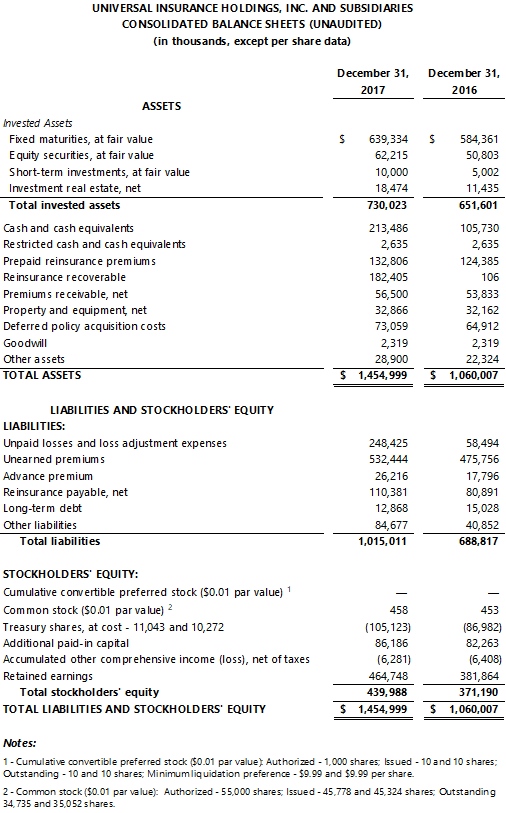

Net investment income grew by 27.5% from the prior year’s quarter to $4.4 million, driven by the increasing size of our investment portfolio, a shift in asset mix, and an increased investment portfolio yield as compared to the prior year’s quarter. Net realized investment gains were $0.1 million in the fourth quarter of 2017, compared to net realized gains of $1.0 million in the prior year’s quarter. Total unrestricted cash and invested assets was $943.5 million at December 31, 2017, growth of 24.6% from $757.3 million at December 31, 2016.

Interest expense was $79 thousand for the fourth quarter of 2017, compared to $59 thousand in the prior year’s quarter, with long term debt of $12.9 million at December 31, 2017 (debt-to-equity of 2.9%), compared to $15.4 million as of December 31, 2016 (debt-to-equity of 4.0%).

The effective tax rate for the fourth quarter of 2017 was 37.9%, compared to 39.9% in the prior year’s quarter. The current year’s quarter includes several discrete items, which in aggregate reduced our income tax expense by approximately $0.2 million, lowering the effective tax rate by 0.3 percentage points for the quarter. Discrete items included a credit to income tax expense of $5.0 million for excess tax benefits resulting from stock-based awards that vested and/or were exercised during the fourth quarter, largely offset by a deferred tax asset (DTA) remeasurement of $4.7 million related to tax reform legislation passed in December 2017.

Stockholders’ equity was $440.0 million at December 31, 2017, growth of 4.6% from September 30, 2017, or 18.5% from December 31, 2016. Book value per common was $12.67 at December 31, 2017, growth of 3.7% from $12.21 at September 30, 2017, or 19.6% from $10.59 at December 31, 2016. Return on Average Common Equity (ROE) was 33.0% for the fourth quarter of 2017 compared to 14.4% for the fourth quarter of 2016, and 25.7% for year ended December 31, 2017 compared to 29.4% for year ended December 31, 2016.

During the fourth quarter, the Company repurchased 10,000 shares for $0.3 million, or an average cost of $25.71 per share. For the year ended December 31, 2017, the Company repurchased 770,559 shares for $18.1 million, or an average cost of $23.54 per share. Our current share repurchase authorization program has $19.8 million remaining and runs through December 31, 2018.

On November 16, 2017, the Company announced that its Board of Directors declared a cash dividend of $0.27 per share of common stock that was paid on December 4, 2017 to shareholders of record as of November 27, 2017. The $0.27 per share dividend included the regular $0.14 per share fourth quarter dividend and an additional special dividend of $0.13 per share. Total cash dividends during 2017 were $0.69 per share, a dividend yield of 2.8% based on the average UVE share price throughout 2017. On January 22, 2018, the Company announced that its Board of Directors declared a cash dividend of $0.14 per share of common stock to be paid on March 12, 2018 to shareholders of record as of February 28, 2018.

Hurricane Irma Overview

Hurricane Irma made initial landfall in the Florida Keys on September 10, 2017 as a Category 4 storm on the Saffir-Simpson Hurricane Scale. Hurricane Irma was an extremely destructive event that caused a wide swath of damage across the entire Florida peninsula and throughout the Southeastern United States. Although Hurricane Irma was a devastating catastrophic event, the ultimate net financial impact to Universal was substantially limited by both our comprehensive reinsurance program and benefits received as a result of our vertically integrated structure. The initial net loss and LAE reported by the Company in the third quarter of 2017 related to Hurricane Irma was $37.0 million. This amount was partially offset by favorable revisions to ceded losses and LAE of $9.2 million during the fourth quarter of 2017 to reflect recoveries related to our Other States Reinsurance Program. Additionally, our service company subsidiaries generated substantial additional revenues following Hurricane Irma that led to approximately $35.0 million of estimated pretax profit generated by service company subsidiaries during the fourth quarter of 2017. In total, for the year ended December 31, 2017, the Company estimates that Hurricane Irma had an aggregate net benefit on its financial results of approximately $7.2 million on a pretax basis. The discussion below provides additional commentary surrounding the various effects of Hurricane Irma on the Company’s financial results.

- Comprehensive Reinsurance Program – During the quarter ended September 30, 2017, the Company recorded gross losses and loss adjustment expenses of $452.0 million resulting from Hurricane Irma, reflecting gross losses and LAE of $450.0 million at Universal Property & Casualty Insurance Company (UPCIC) and $2.0 million at American Platinum Property and Casualty Insurance Company (APPCIC). The Company’s reinsurance protection performed as expected, reducing exposure to the maximum retention limits, limiting net losses and loss adjustment expenses from Hurricane Irma to $37.0 million. During the quarter ended December 31, 2017, the Company revised its estimated gross losses and loss adjustment expenses to $447.0 million, reflecting gross losses and LAE of $445.0 million at UPCIC and $2.0 million at APPCIC, which had no effect on the Company’s net loss retention. This revision to gross losses at UPCIC was to account for claims experience during the fourth quarter, and we note that as of February 9, 2018, the Company has received 68,634 claims relating to Hurricane Irma, of which 57,799, or approximately 84%, have already been closed. Because gross losses and LAE in states outside of Florida are projected to be $12.8 million (which is above our $5.0 million Non-Florida retention) additional recoveries from our Other States Reinsurance Program during the fourth quarter served to reduce UPCIC’s aggregate retention from $35 million to $27.2 million. After adding in APPCIC’s net retention of $2.0 million, this resulted in a total net retention of losses and loss adjustment expenses of $29.2 million related to Hurricane Irma for the year ended December 31, 2017. Additionally, the Company experienced approximately $2.4 million of gross losses and loss adjustment expenses related to hailstorms in Minnesota that occurred in June of 2017. As a result of Hurricane Irma satisfying an otherwise recoverable provision within our Other States Reinsurance Program, the Company’s retention in states outside of Florida was reduced to $1.0 million from $5.0 million. This resulted in an effective savings of $1.4 million recorded in the fourth quarter of 2017 on the Minnesota hailstorm events, as the Company retained only the first $1.0 million of losses on the event. Through May 31, 2018, our Other States Reinsurance Program will continue to have a net retention of $1.0 million as a result of the otherwise recoverable provision having been satisfied.

- Vertically Integrated Structure – As we have previously disclosed, the Company benefits from our vertically integrated structure by retaining certain revenues and/or fees that are paid to our subsidiary service providers for various services provided, including reinsurance brokerage, claims adjusting and other services. This benefit is particularly notable during large catastrophic events such as Hurricane Irma, which result in a substantial number of claims leading to increased activity at our service company subsidiaries. As a result of Hurricane Irma, the quarter and year ended December 31, 2017 included the benefit of additional net revenues within our service provider subsidiaries, particularly Universal Adjusting Corporation (UAC) and Blue Atlantic Reinsurance Corporation (BARC), which led to a higher level of profitability than would otherwise be the case in a normal quarter or year. In aggregate, the company estimates that these additional revenues at service company subsidiaries resulted in approximately $35.0 million of net pretax benefit during the fourth quarter and full year 2017. This favorable benefit related primarily to two factors: (1) as a result of the increased level of claims following Hurricane Irma, UAC, which manages our claims processing and adjustment functions, experienced a significant increase in net revenues and net profit in the months following the storm, and (2) Commission Revenue included a benefit of approximately $2.0 million related to reinstatement premium commissions received by BARC.

- Other Factors – In addition to the items discussed above, Hurricane Irma resulted in various other effects on our ongoing business, in particular with respect to premium writings and policy fee income. We experienced an increased level of premium volume, including an increase in both new and renewal business, as well as a corresponding increase in policy fee income, during both the quarter ending September 30, 2017 and the quarter ending December 31, 2017. Several days after Hurricane Irma made landfall, the Florida Insurance Commissioner issued an emergency order that temporarily suspended policy cancellations and nonrenewals by insurance companies. Specifically, the order barred insurance companies from cancelling or nonrenewing policies between September 4, 2017 and October 15, 2017; barred the cancellation or nonrenewal of policies covering residential properties damaged by Hurricane Irma until at least 90 days after the properties are repaired; and required that any cancellations or nonrenewals issued or mailed from August 25, 2017 through September 3, 2017 were withdrawn and reissued no earlier than October 15, 2017. This emergency order resulted in increased levels of premium and policy fee volume as compared to both the prior year and our internal expectations. In addition, the emergency order resulted in a delay of our previously filed FL statewide rate increase (which was for an average statewide increase of 3.4%). We had initially expected our rates to be approved by the Florida OIR in September, and as a result of Hurricane Irma and the corresponding emergency order, the rates were not approved until early December. We began using our new rates on December 7, 2017 for new business and on January 26, 2018 for renewal business.

Conference Call

Members of the Universal management team will host a conference call on Wednesday, February 21, 2018 at 10:00 AM ET to discuss fourth quarter 2017 financial results. Following prepared remarks, management will conduct a question and answer session. The call will be accessible by dialing toll free at (888) 887-7180 or internationally (toll) at (270) 823-1518 using the Conference ID: 9892307. A live audio webcast of the call will also be accessible on the Universal Insurance website at www.universalinsuranceholdings.com. A replay of the call can be accessed toll free at (855) 859-2056 or internationally (toll) at (404) 537-3406 using the Conference ID: 9892307, and will be available through March 8, 2018.

About Universal Insurance Holdings, Inc.

Universal Insurance Holdings, Inc., with its wholly-owned subsidiaries, is a vertically integrated insurance holding company performing all aspects of insurance underwriting, distribution and claims. Universal Property & Casualty Insurance Company (UPCIC), a wholly-owned subsidiary of the Company, is one of the leading writers of homeowners insurance in Florida and is now fully licensed and has commenced its operations in North Carolina, South Carolina, Hawaii, Georgia, Massachusetts, Maryland, Delaware, Indiana, Pennsylvania, Minnesota, Michigan, Alabama, Virginia, New Jersey, and New York. American Platinum Property and Casualty Insurance Company (APPCIC), also a wholly-owned subsidiary, currently writes homeowners multi-peril insurance on Florida homes valued in excess of $1 million, which are limits and coverages currently not targeted through its affiliate UPCIC. APPCIC is additionally licensed and has commenced writing Fire, Commercial Multi-Peril, and Other Liability lines of business in Florida. For additional information on the Company, please visit our investor relations website at www.universalinsuranceholdings.com.

Forward-Looking Statements and Risk Factors

This press release may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. The words “believe,” “expect,” “anticipate,” and similar expressions identify forward-looking statements, which speak only as of the date the statement was made. Such statements may include commentary on plans, products and lines of business, marketing arrangements, reinsurance programs and other business developments and assumptions relating to the foregoing. Forward-looking statements are inherently subject to risks and uncertainties, some of which cannot be predicted or quantified. Future results could differ materially from those described, and the Company undertakes no obligation to correct or update any forward-looking statements. For further information regarding risk factors that could affect the Company’s operations and future results, refer to the Company’s reports filed with the Securities and Exchange Commission, including Form 10-K for the year ended December 31, 2016 and Form 10-Q for the quarter ended September 30, 2017.

Contacts

Investors

Dean Evans

VP Investor Relations

954-958-1306

de0130@universalproperty.com

Media

Andy Brimmer / Mahmoud Siddig

Joele Frank, Wilkinson Brimmer Katcher

212-355-4449